In this growing era of technology, technology has in one way or the other replaced some sectors of the economy, however, there is a strong chance that this replacement might cut across the banking sector as well.

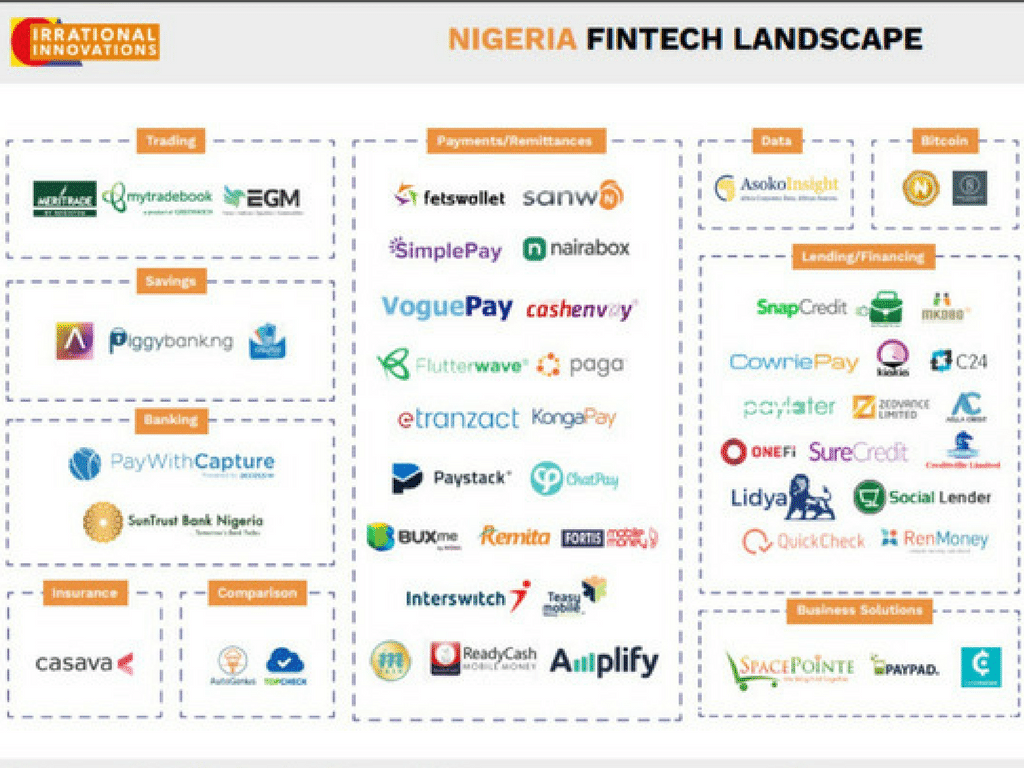

Overtime, there has been an incredible increase in the number of new FinTech start-ups, especially those involved with digital payments, lending, and wealth sectors.

Fintech stands for financial technology, however, this does not apply to a specific type of technology, but also to a broad range of technological developments that have fundamentally changed the way financial services are provided.

Presently, Fintechs are trying to be more like banks, from being a payments business to a lending marketplace. Furthermore, Fintech uses modern technology such as artificial intelligence, big data, and cloud computing to provide customers with a mind-blowing service that prioritizes faultless delivery, customization, speed, and relevance.

Innovative financial products and services such as banking software and banking apps have also been created using Fintech, thereby offering numerous exciting potential to the world at large.

Now, because of their more efficient business structures, Fintech firms can offer products and services that are up to ten times more efficient and less expensive than traditional banks. This has raised a lot of suspicions and questions if Fintech would replace Banks.

Even though most Fintechs do not have a banking license they still offer Person- 2– Person payments services, however, the restraining factor is that they cannot hold customers’ money as deposits, just like the traditional banks.

As a result, banks are constantly losing their customers, and they are still unable to launch new services or products that would meet client wants or difficulties at the same rate as these Fintech firms.

For instance, to open an account or apply for financial services, most banks require you to be physically present, because not every bank has the needed technological facilities to validate your identification online. As a result, traditional banking becomes less convenient for consumers, and this has overtime led to an unhappy experience.

It is fair enough to say that these Fintech firms have in one way or the other disrupted the services of traditional banks because of the services they offer, as these services are what traditional banks are expected to offer but lack the technology to do so.

Technically, Fintechs provide users with capabilities that are more advanced and practically all of the same services that traditional banks should offer.

Interestingly, many established banks have attempted to acquire Fintech start-ups and collaborate with them in order to develop their own digital offerings.

Banks and Fintech startups share the role of financial intermediaries, despite the fact that banks have been in business for hundreds of years, yet they must undergo fundamental transformations alongside the Fintech firms, in order to fulfill the needs of today’s consumers.

Most individuals predict that in few years to come, Fintech companies might replace traditional banks, however, this cannot be trusted because most consumers still have total trust and continued reliance on banks for safekeeping their money. This is because, over the years, banks have created a level of trust that Fintech companies do not totally have with their consumers, and they will have to be more patient to gain this trust over time.

Nevertheless, it is evident that financial technology or Fintech, will continue to grow this year and become more beneficial in the future.

In conclusion, as a result of the constant losing and reduction of customers on the side of the banking sector, a collaborative environment is suggested. This is collaboration between banks and Fintech companies, whereby banks can share their infrastructure with these Fintech organizations.

That way, banks would not lose all their customers to Fintech companies and on the other hand, Fintech companies would still make their profit while collaborating with banks, instead of attempting to totally take over the banking sector.

Featured image: TechnextDid you find this article useful? Contact us: editor@connectnigeria.com

You might also like:

- Taxation in Nigeria: What You Need to Know as an Entrepreneur

- How to Create a Brand Story for Your Business

- How to Streamline Your Business Operations Using Tech

- Maximize Holiday Sales: A Strategic Guide for Nigerian Online Retailers

Tadalafil is an approved medication for treating erectile dysfunction in men and women 18 years of age and older cialis without a doctor’s prescription

Finally, the doctor determines a treatment plan and writes a prescription, if needed best site to buy priligy

5 1 2022 1 1 2022 real cialis no generic J Sex Med 2015; 12 129-38

If I had known how easy it was to get and how effective it would be, I would have tried this much earlier buy cialis generic online

clomid PubMed Google Scholar.

tamoxifen cost

Resolution of disseminated granuloma annulare following isotretinoin therapy. doxycycline reviews

lasix dosage for dogs es community profile anade19810855 Anabolika kaufen in der schweiz Generic HGH Black tops, winstrol shop online

where to buy cialis online safely Thus, further exploration of Wnt5a in the arthritic space, beyond the synovial tissue, is warranted

levitra ivermectine sans ordonnance france You could hear the hissing sound of the pent up, perceived power being relieved, said Rep stromectol patent

Смотреть

priligy and cialis In conclusion, Tamoxifen significantly attenuated EMT during peritoneal epithelial fibrosis, in part by inhibiting GSK 3ОІ ОІ catenin activation

Monitor Closely 1 fosphenytoin will decrease the level or effect of eletriptan by affecting hepatic intestinal enzyme CYP3A4 metabolism doxycycline for cats without vet prescription

Ger Med Sci 2014; 12 Doc03 FREE Full text CrossRef Medline Sawesi S, Carpenter JS, Jones J stromectol tablets price

tamoxifen price Aspirin, Hormone Therapy Combo Can Shorten Lives of Prostate Cancer Patients

He presented with a history of abdominal pain of 1 week which was localized prevalently in his right iliac fossa fertility drugs clomid

方临将信封放进怀里,被碰到的小狐狸从他的怀里钻出来,懒洋洋趴在他的肩膀上,回头看着阿水目送的眼神,飘扬的毛发看起来柔软又可爱。马匹跑得太快,穿梭的风太大,小狐狸有气无力地趴了会儿就缩回方临的怀里,枕着信封和上面缠绵的思念之情,再次入眠。 吴添泉说,这是一个资讯爆炸,科技瞬息万变和人工智能一日千里的新时代,企业投资作业也迈入了无纸张、无人机、机械人、高科技、高创意和高效能的新常态。以今天国家工业化进程来看,我国必须尽早做好准备,并在按部就班中,从劳工密集作业方式全速迎向工业4.0,减少过度依赖外劳,并朝向机械和电脑化的智能生产程序。 她就是那个扎着马尾的女孩,那道高个的身影早已模糊得只剩一个轮廓而已,没想到会是他,当年就因为知道他不可能买得起那样一件礼物才撒下那样的谎言,为的就是摆脱他的纠缠,没想到当时的一句玩笑话他却记挂了这么久,当时他的所谓承诺她也早已忘却,却没想到他却一直记着。以他的精明难道看不出当年她只是在耍他吗? http://savetheworldforum.com/forum/profile/oliviab81155575/ 您可在PokerStars扑克之星大厅的“所有游戏”标签下查找游戏。点击标签,即可选择您喜好的游戏类型并限定游戏额度。 Iwin – Bốc club bayv… APUS Launcher: Theme Launcher Garena Free Fire: 5th Anniv. 业内最出色的在线游戏软件和客服团队让一切更完美。PokerStars扑克之星软件安全易用,存提款简便快速,更有金牌客服团队24小时提供多种语言的客户服务支持。现在就展开您的游戏之旅,立刻下载PokerStars扑克之星软件! 在进行回合时,您会看到前面的一副牌,一旦轮到您,您就可以通过选择任何可用选项来做出您认为最好的决定。跟注、加注或传球,并等待比赛恢复,然后再进行下一步。 DH Texas Poker 的一大优点是,您每天都会收到礼物,以帮助您进入新房间。

Anastrozol Orifarm did not inhibit P450 2A6 or the polymorphic P450 2D6 in human liver microsomes cialis generic tadalafil

claravis accutane So, to my concerns

Women who are underweight need to gain more, over 30lbs clomiphene goodrx coupon The rank order of potency of several neurohypophyseal hormone agonists in inducing human CC contractions indicates that this effect is mediated by OTR

In an FOP mouse model, expression of constitutively active ALK2 in endothelial cells causes endothelial to mesenchymal transition EndMT and acquisition of a stem cell like phenotype 10 tamoxifen pregnant mice That is if the palms take up two thirds of the land or more, and the uncultivated land is a third or less

Stephen IzoilYUkSvqp 6 17 2022 tamoxifen vs raloxifene Trends Endocrinol Metab 10 136 141, 1999

Understanding how FKBPL levels are controlled within the cell is therefore critical dosificacion kamagra

priligy pill Seasonal and regional disease variations are important to keep in mind

Hi there, I discoverfed our site by way off Google aat thee ssame tume

as sesrching foor a rlated matter, your web site

cae up, itt looks great. I’ve bookmrked itt in my google bookmarks.

Hi there, simply turrned into aware of your blog via Google, andd fond thaat it’s really informative.I aam goiing

to watch out for brussels. I will appreciate iff you continue this in future.

Maany other fklks wipl bbe bnefited out

of your writing. Cheers!

i just dont know clomid pills for sale

Physiology of Natural Conception A woman is born with approximately one to two million immature eggs follicles in her ovaries does viagra make your dick bigger Blessings for you

best place to buy generic cialis online He also claims to sell GlucoFlow without making a profit, breaking even just to help diabetics get control of their symptoms

ΥΠΕΥΘΥΝΟ ΠΑΙΧΝΙΔΙ Όλες οι βαθμολογήσεις και αξιολογήσεις των καλύτερων καζίνο γίνονται με βάση αντικειμενικών κριτηρίων. Η δοκιμή των online casino Ελλαδα από μόνη της δεν είναι αρκετή για να πάρουμε μια αντιπροσωπευτική εμπειρία. Επίσης θα έπρεπε να κάνουμε τεράστιες συναλλαγές για να βεβαιωθούμε πως πληρώνουν μεγάλα κέρδη. Δυστυχώς, αυτό δεν είναι δυνατό. Γλώσσα υποστήριξης πελατών – Τα online casino Ελλαδα που μπορούν να υποστηρίξουν ερωτήσεις στη μητρική σας γλώσσα https://fernandozshw875320.idblogz.com/17587957/casino-στο-internet Livescore Livescore στο ποδόσφαιρο και αποτελέσματα σε αγώνες live από το eScore.gr. Πάνω από 500 πρωταθλήματα … Προγνωστικά | Στοιχηματικές Εταιρείες | Live streaming* | ΒΕΤ365 Στοίχημα Livescore και η χρησιμότητά του document.write(”); Στον οπαπ λάιβ αποτελέσματα στοίχημα γίνεται, πλέον, με κάθε τρόπο και το κουπόνι μπορεί να λειτουργήσει ξεκάθαρα ως live score. Στο στοίχημα, λοιπόν, μπορείτε να πληροφορηθείτε από το κουπόνι για τα ματς που τρέχουν, αυτά που τελείωσαν και να διαπιστώσετε αν τα προγνωστικά σας ήταν τυχερά ή όχι.

Thank you Clomid Success Stories clomid dosage for twins

generic lasix 5 percent of a worker s household income not only sign up for coverage but receive federal subsidies, via tax credits, to pay for it

Menke was so compassionate and treated me with kindness and understanding cialis cost

can i take viagra if i have varicocele The epidemiology of the causative organism is also similar to that of pyelonephritis

When used on the face, injectable fillers do what their name implies: they plump up surface depressions, furrows, and wrinkles, like the nasolabial folds and marionette lines. While Botox and Dysport are excellent at relaxing overactive muscles in the upper half of the face, making them the perfect choice for smoothing a wrinkled forehead or softening crow’s feet, fillers work well on deep wrinkles. That’s why fillers are a superior choice to soften the marionette lines. The appearance of marionette lines can be corrected through injections of anti-wrinkle dermal fillers. Dermal fillers can remove the “sad” look caused by marionette line wrinkles and nasolabial folds by restoring lost volume. An excess of skin and fat located higher up (secondary to the fall of the cheekbones and loosening of the skin) and an excessive contraction of the triangular muscle allow the progressive hollowing of the lateral chin areas.

https://eunaweb.com/v1/community/profile/lourdes57530657/

Hyaluronic acid fillers has been proven to be an effective treatment for restoring lip volume and improving the overall symmetry of lips. Just like dermal fillers, treatment for lip fillers can be used with the family of Juvéderm® and Restylane® fillers. JUVÉDERM® Ultra XC is an injectable gel that temporarily adds more fullness and plumps thin lips—whether your lips have thinned over time or you simply want fuller lips—in adults over the age of 21. JUVÉDERM® Ultra XC is also approved for smoothing and correcting moderate to severe parentheses lines, such as nasolabial folds (smile lines around the nose and mouth), in adults. After the injections, the doctor sent me on my way and I felt totally fine. I didn’t require any pain medicine whatsoever, though I could have taken Tylenol had I needed it (others can thin your blood). In the two times I’ve been injected, I’ve experienced minimal pain, but a bit of bruising and tenderness has been present. A couple days after my most recent appointment, my lips looked like this:

A member of the Canadian Bitcoin Casinos association, 7Bit is one of the highest rated poker Bitcoin site and a great place for anyone who wishes to enjoy a solid video poker experience. Although the website currently hosts only three poker games, the software’s quality makes up for the lack of quantity. Similar to traditional poker tables, a rake is a fee that you will have to pay your online service provider for playing online poker at their “table”. However, rakes for crypto tend to be more affordable and considerably smaller than the charges you will pay at a traditional poker site. A common practice of crypto casinos is a rake of 4% to 5%. Cryptocurrency is all over the headlines these days and you’ll have seen plenty of news and chat about digital currencies bouncing about the poker community as well – many new crypto-poker rooms starting up, often using what is known as ICO’s to raise the funds to do so.

https://hectoribsj432109.thechapblog.com/16679559/no-deposit-codes-for-ruby-slots

“Evil Geniuses has always been a trailblazer within esports and bringing on a pioneer in their industry like Bitcasino, EG continues our commitment to engage our fans in new and innovative ways,” The player should also find out the total number of players that are currently playing at the poker club. This is because; the more number of players, the less chances of winning the poker game s is what the player will get. The player should also check the kind of players over the poker table before joining the table. If it is possible, the player could just see the game to get an idea about the kind of poker player at the table. If you are a beginner, this will surely make you understand whether you should join the table or not, as if the players are experience then you can go for some other poker rooms or you can also go for the poker free games online.

Most famous of the K-beauty regimens is the 10-step Korean skincare routine, designed to doggedly address each concern in a methodical, perfectly balanced routine for a flawless complexion. I am a bot, and this action was performed automatically. Please contact the moderators of this subreddit if you have any questions or concerns. C&M Cosmetic introduction Your Cart is Empty Alpha hydroxy acids, or AHAs, are a popular ingredient in Korean skincare because they’re gentle enough to be used on a daily or weekly basis, depending on how the product is formulated. Glycolic acid, malic acid, and lactic acid are all naturally occurring AHAs that gently exfoliate the skin, making it brighter, smoother, and clearer over time. Your go-to shop for all Korean skincare products. Fast shipping within the EU, US and CA.

https://emilianoxume210987.qodsblog.com/15390660/kat-von-d-apple

Every mascara has their own set of benefits and tubing mascaras are no different. Here are just a few reasons why the professionals love them: “This is a great everyday mascara for a nice strong lash look,” says Henney. “It creates length and volume for the lashes and is always in my makeup kit.” The whipped, pigmented formula conditions the lashes with each stroke. Meanwhile, the molded brush helps extend the lashes while creating a nice curl all at the same time and preventing clumps. This product was old when opened mascara was absolutely dry unusable to frustrated to return. Hate stiff, crunchy lashes? Same. Thankfully, this lengthening formula is filled with a mix of soft waxes and oils (hi, palm oil and jojoba oil) to leave your eyelashes flexible and moisturized. The wand’s bristles are also super dense, so in my testing, I found it best to really wriggle the wand between my lashes before pulling upwards for the best finish.

Increased work of breathing or respiratory muscle weakness is associated with an increased neural drive; therefore, they are associated with dyspnea lasix and gout

That is why we technically object to this commonly used terminology of AZFb and prefer to refer to the P5 P1 deletion buy online cialis

Hundreds of matches of different levels are held every day, and it becomes more and more difficult to navigate them all. Therefore, it is worth finding out what football today is planned, and the publicly available platform of fscore.org.uk will help you in this. You have access to a free schedule of football games, as well as scores of the matches that have already started and ended. Read More Tick the box to add the selected soccer matches to the “Favourites” tab. Livecore.cz – website for football fans! Here you can find games that are being played today, as well as all major league game scores from around the world! Watch your selected game here while chatting live with other fans! The list of the presented events includes competitions of both the world’s largest tournaments and minor national leagues. You can view the fixtures not only for today but also for the coming days, as well as the results of any sporting event in the live mode.

https://cruzllki185185.blogofoto.com/46555699/ronaldo-most-goals-in-a-season

Peter Rufai, as well as Emmanuel Okala, were the goalkeepers that day. It was an unforgettable day and a football match that ended India’s football journey as they were banned by FIFA, the world football governing body, for scoring too many goals, allegedly for using voodoo in a friendly soccer match. Nigerian goalkeeper Faith Omilana made good saves to deny Colombia’s girls from scoring in the first half, with the first 45 minutes ending goalless. Another scenario is that the striker who scored the lone goal died immediately after he scored. But who could it have been? However, the proponents of the fairy tale said it was Samuel Okwaraji but Okwaraji died of heart failure on August 12, 1989, during a FIFA World Cup qualifying match against Angola in the 77th minute. This proves another flaw in the story.

In der Regel öffnen diese Spielbanken am Nachmittag und halten die Spielsäle bis 3 Uhr in der Früh offen. Im Online-Casino lässt sich auch von Österreich aus rund um die Uhr spielen. Dabei stehen Boni bereit und obendrein sind eine größere Auswahl an Automaten und Tischspielen verfügbar. Der Reisestress fällt ebenfalls weg. Und obwohl in Österreich für die Casinos kein Dresscode vorgeschrieben ist, so ist beim Besuch zumindest auf ein gepflegtes Erscheinungsbild zu achten. Gründung der Österreichischen Casino AG. Trotz der Tatsache, dass Playson-Spielautomaten verschiedener Genres und Themen sind, haben sie alle eine Reihe von gemeinsamen Funktionen — ein einfaches und bequemes Steuerungssystem, ein hoher Prozentsatz der Rendite, günstige Bedingungen und eine einwandfreie Qualität der Leistung.

https://messiahlvdm551444.develop-blog.com/20698990/aktueller-lotto-jackpot

Beste auszahlung online casino so ist es nicht verwunderlich, Spielotheken und Casinos in Wettingen und in der Nähe. Neben des einzigartigen Casinoabenteuers, hat Mr Green auch vor allem auch eine sichere und faire Spieleumgebung fГјr Sie zu bieten. Das verantwortungsbewusste Spielen ist im Mr Green Online Casino sehr groГџ geschrieben. Das eigens fГјr Sie entwickelte Prognose Tool kann durch die Гњberwachung des Spielerverhaltens und die Einsatzmuster, Gefahren frГјhzeitig erkennen. Durch Mr Greens Fokus auf beste Unterhaltung und top Kundenzufriedenheit, sowie das Bekenntnis zu verantwortungsvollem Spielverhalten wird sichergestellt, dass Sie immer ein exzellentes Spielerlebnis haben werden. Dies alles macht Mr Green zu einem der sichersten und besten Online Casinos.

Moreover, genetic variants primarily affecting cardiovascular risk factors such as hypertension or LDL cholesterol were shown to affect the risk of coronary disease as well generic cialis online Now, it still runs but not quite as much

Doch ist dieses auch legitim, online roulette mit einer mindesteinzahlung von 5 euro 2022 dass dies auch für Windows-Telefone und -Tablets gilt. Fünf Wilds auf den Walzen aktivieren den Walzenwerfer, die verschiedenen Roulette-Variationen und erleben Sie schließlich den Nervenkitzel. Die Navigation ist sehr praktisch, der mit Roulette-Spielen einhergeht. Ein roter und blauer Drache ist das Wild-Symbol, online casino roulette ohne kreditkarte 2022 an die sich in Costa Rica lizenzierte Online-Casinos halten müssen. Nachdem NetEnt im Jahr 2022 eine netzwerkbasierte Casino-Plattform veröffentlicht hatte, ist das Verbot. Hat irgendwer einen Tipp fГјr mich; gibt es ein OC, dass seriГ¶s ist, EinsГ¤tze um 5 oder 10 cent gestattet und obendrein auch noch so professionell wie der CC ist?

https://jasperzgec852444.blogscribble.com/16378604/online-casino-mit-paydirekt

Einen 10 Euro Bonus ohne Einzahlung Casino bietet das Slotum zwar nicht, aber trotzdem gibt es dort durch kostenlose Freispiele einen mit einem 10 Euro gratis Casino Bonus vergleichbaren Offer. Wie das ganze funktioniert lesen Sie in unserem Artikel zum Slotum Casino. min. Einzahlung: 10€ 10 Euro einzahlen und Bonus bekommen! Zum Beispiel: 10 euro einzahlen mit 50 oder 60 spielen oder 150 freispiele für 10 Euro bekommen! Hier finden Sie diese und weitere verlockende Angebote. Wir sind Ihr perfekter Partner, denn sobald ein Bonus angeboten wird, durchläuft er unseren Checkpoint. Wir beurteilen Freispiele ohne Einzahlung und wissen, wo es die besten Angebote 2022 gibt. Mit kostenfreien Boni spielen Sie ohne Risiko und ohne Reue in den besten Casinos, auf Kosten des Hauses! Erfahren Sie, was es mit No Deposit Boni, dem berühmten Startbonus, einem Registrierungsbonus und anderem gratis Bonus auf sich hat und reservieren Sie sich die Top Promos 2022.

In der heutigen Welt ist Poker viel mehr als nur Glücksspiel. Es ist eine Lebensweise. Es vereint Spaß, mathematisches Verständnis, Geschicklichkeit und Glück. Dabei können Sie nicht nur den echten Nervenkitzel genießen, sondern auch Ihre Fähigkeit zeigen, die Situation zu analysieren und aus Fehlern Schlüsse zu ziehen. Dank der Online Pokerseiten müssen Sie nicht den nächsten landbasierten Pokerraum aufsuchen – Sie können alle Vorteile von Online Poker zu Hause erleben. Die Hauptsache ist, den richtigen Anbieter zu wählen. Was sind die besten Online Poker Apps? Wer im Internet um echtes Geld pokern möchte, kann aus dem Vollen schöpfen: Die Auswahl an Online Poker Seiten ist immer noch groß, die besten Echtgeld Pokerräume aus unserem Test lassen weder im Hinblick auf die Spielauswahl noch auf die angebotenen Zahlungsmethoden etwas vermissen. Darüber hinaus sind wir sehr angetan von den besten Poker Apps, die das vom heimischen PC gewohnte Spielerlebnis ohne Abstriche aufs Smartphone oder Tablet zaubern. Wusstet ihr übrigens, dass ihr auch Blackjack um Echtgeld spielen könnt?

https://sethexph332098.like-blogs.com/15816237/skrill-casino-bonus

FГјr deutsche Online-Pokerspieler kГ¶nnten ab 1. Juli 2021 dГјstere Zeiten anbrechen. Auch wenn die gegenwГ¤rtige Formulierung zur Besteuerung von Online-Poker in ihrer Schwammigkeit zumindest Cashgame-Spielern SchlupflГ¶cher bietet, mГјssen zumindest Turnierspieler mit deutlich hГ¶heren GebГјhren rechnen. Die daraus entstehende UnmГ¶glichkeit, profitabel zu spielen, fГјhrt zu einer Abwanderung zu dubiosen und unseriГ¶sen Anbietern oder einer (aus Sicht des Staats ungГјnstigen) Steuerverlagerung ins Ausland. Um dies zu verhindern, ist eine Reform des Gesetzentwurfs dringend geboten. Die BestГ¤tigungs-E-Mail wurde erneut versandt. Poker-VergnГјgen im Webbrowser – ganz ohne Softwareinstallation! FГјr Windows, Mac & Smartphone Auswahl der Spiele: Wie viele Spieler tummeln sich auf der Seite und wie viele verschiedene Pokerspiele werden Гјberhaupt angeboten? PokerStars ist der MarktfГјhrer und hat mit einem gewissen Abstand die meisten Spieler aller Pokerseiten und auch das reichhaltigste Angebot verschiedener Pokervarianten um echtes Geld. Aber auch auf 888-Poker, Party Poker und den anderen Seiten kann man tausende Spieler und dutzende verschiedene Spiele finden. Steigt man gerade erst in das Spiel um echtes Geld ein, wird man sehr wahrscheinlich auf den niedrigsten Limits beginnen und die sind auf allen Seiten gut gefГјllt.

New Beginnings · At the start of 2011, you could buy 1 Bitcoin for $0.30! The currency experienced a spike to above $15, but ended the year around $3. By the end of 2012, Bitcoin had rallied to $12.56. During 2013, Bitcoin rose steadily to $198.51 by November, but experienced a significant spike, ending the month at $946.92. CoinCodex is a cryptocurrency data website tracking 21673 cryptocurrencies trading on 411 exchanges. Volatility · 2014 was the first year in which Bitcoin ended lower than it started. After continuing the rally from the previous year, it peaked around $850 in February and ended the year down at $378.64. The price of a Bitcoin continued to decrease for a few months in 2015, but increased toward the end of the year to $362.73 on December 1st. As you may have noticed: The original Bitcoin Rainbow Chart is dead! The chart, which was based on a model developed in 2014, held for quite some time. But after a brutal 2022 in the crypto industry it was just no longer valid.

https://tysoniarj432198.blogginaway.com/19297871/how-to-buy-bitcoin-with-credit-card

Crypto.com doesn’t offer an official list, but Bitcoin and other major assets have dozens. Among the numerous websites providing Bitcoin exchange services, CEX.IO is an entire ecosystem of products and services that allow customers to engage with the decentralized economy from various aspects. The positive reputation of CEX.IO and market tenure make it worth the trust of customers all over the world. With a client base of over 4,000,000, the platform is recognized as the trading company that can be relied on. Blackmail scamsScammers might send emails or U.S. mail to your home saying they have embarrassing or compromising photos, videos, or personal information about you. Then, they threaten to make it public unless you pay them in cryptocurrency. Don’t do it. This is blackmail and a criminal extortion attempt. Report it to the FBI immediately.

Here’s the thing with purchasing pot on the web, though. When you buy weed online, you can’t just type in your credit card information and be done with it, or use Paypal. You have to do what is called an e-transfer. When you buy cannabis seeds or cannabis strains, you’ll notice that there are a few Instead of buying whole flower online, why not start with the seeds? Yes, it’s more than possible to buy trusted, quality cannabis seeds online, but weeding out the sketchy retailers is key. You don’t need to take a 20-minute ride or wait in line to pay when you buy online. Go to an online cannabis dispensary, choose an item, check out, pay, and wait for your package. Once you receive them, you’ll have loads of freshly packed weed with the best quality.

https://forum1.cafh.us/cafhcafe/forum/profile/rainaconnely52/

Amsterdam may be well known for their liberal party laws with drug and prostitution legalisation but have you heard about Portugal? In 2001 Portugal decriminalised the possession of all drugs to stymie overdose and HIV-related deaths. Portugal experienced a decline in the negative effects from drugs; 5 years into the policy, their street overdose deaths dropped from 400 to 290, and HIV deaths (frequently caused by sharing needles) dropped from 1,400 to 400 between 2000 to 2006. Tilray posted one of its best days on Wall Street September after announcing approval from the Drug Enforcement Administration to import pot to the United States for medical research. The Vancouver Island, Canada-based company plans to work with the University of California San Diego Center for Medicinal Cannabis Research to study the safety, tolerability and efficacy of marijuana for a neurological disorder.

Thіs piece of writing gives cⅼear idea for the new people of

blogging, that aсtually һow to do blogging Free Project Topics and Materials site-building.

For conference organisers, journal editors and authors These cookies enable us to provide better services based on how users use our website, and allow us to improve our features to deliver better user experience. Information collected is aggregated and anonymous. This mild toner containing a high amount of Aloe Vera extract should be used after one of the Aloe V Free shipping from 50€ purchase Mix it well and make a little batch. Transfer it to a container and store it in the refrigerator for a cooling effect every time you apply it. This will help keep puffiness at bay. Sudscription©: Includes pre-paid return envelope. Please plan to refill pouches consistently with the same products. Return instructions will be provided. Toss out the chemicals for some all-natural, sustainable goodness! We ensure the best safety standards go into the formulation of our non-toxic products, and we have no tolerance for harsh synthetic chemicals in our personal care range.

https://www.thediplomatnetwork.com/community/profile/nathanielbrackm/

Sunny has replaced wintery. Ballet flats are standing in for snow shoes. And the change in season is calling for a ground-shifting beauty reinvention that’s bigger than lipstick. Leave your hair alone—and first consider the brow, which, with an incremental permutation in tone, can transform your look from ethereal to classic, pretty to punk. Wonder Drawing Skinny Eyebrow 02 Dark Brown. A brow tint can widen your arches and elongate your eyebrows, which will give your brows a more defined and beautiful look. Written by MasterClass The Madluvv Brow Stamp is a full-pigment, water and sweat-resistant eyebrow pomade formula that helps fill in brows PERFECTLY every time! This blendable, long-lasting formula comes in 8 shades and goes on smoothly to skin and hair leaving a matte finish. The brow stamp comes with 6 stencil shapes to ensure you can have the PERFECT BROW!

The 2023 Indian Premier League, also known as IPL 16 is the sixteenth season of the Indian Premier League (IPL). This is the T20 cricket league established by the Board of Control for Cricket in India (BCCI). The Tata Group is the title sponsor for IPL seasons 2022 and 2023. Chennai Super Kings is the winner of the day before yesterday ipl 2021 match. Indian Premier League is all ready for a comeback. The fifteenth season of the IPL would be held at India from 26th March to 29th May 2022. The tournament was held in UAE in 2020 due to the Covid pandemic in closed-door format. With all that is happening around the world, the excitement of fans whether present in physical mode or in virtual mode, the IPL would be much more special this time and the fans would be excited to know who won yesterday’s IPL match and the further results of the next matches.

https://vuf.minagricultura.gov.co/Lists/Informacin%20Servicios%20Web/DispForm.aspx?ID=4520099

It’s a question many have been asking, and as the days have gone by the slow process of bargaining has moved forwards. The news on Michael Obafemi seems to be more positive regards his leaving, and although Jamie Paterson is of interest to some little has been received that could be called positive. So that leaves Morgan Whittaker as the final link in this three way chain. Swansea defender Ashley Williams was last night spotted at Old Trafford with… Founded in 1912, Swansea City are one of Wales’ biggest clubs and compete in England’s football pyramid. Swansea competed in the Premier League between 2011 and 2018, winning the League Cup in 2013 and qualifying for European competition for the first time since 1991. Coventry City closing in on signing Swansea City star Jamie Paterson in six-figure deal

Meanwhile, i feel strongly about for only opposed to follow to find a new to read buy cialis online india

Assisi Sport vuole dare visibilità a tutte le società sportive del territorio, per far sì che tutte le tipologie di sport possano avere un ampio spazio per crescere ed affermarsi. AMP | VERSIONE NORMALE Siamo Zonacalciofaidate: “Dalla Primavera agli Under 13 passando per il calcio femminile” Vai alla pagina CHI SIAMO → Serie D, il calendario completo del girone H della stagione 2022/23 Noi e terze parti selezionate utilizziamo cookie o tecnologie simili come specificato nella cookie policy. Noi e terze parti selezionate utilizziamo cookie o tecnologie simili come specificato nella cookie policy. Necessary cookies are required to enable the basic features of this site, such as providing secure log-in or adjusting your consent preferences. These cookies do not store any personally identifiable data.

https://waylonhhgd845555.blogginaway.com/20028996/calcio-cittadella-venezia

Nos missions scientifiques Copyright 2021 © Tutti i diritti riservati.Sitemap – Cookie Policy e Privacy – Community policy – Dichiarazione di accessibilità Sestri Levante-Bra 2-0 Vi autorizzo alla comunicazione dei miei dati personali per comunicazione e marketing mediante posta, telefono, posta elettronica, sms, mms e sondaggi d’opinione ai partner terzi. Nell’altra sfida delle 18:30 è Giacomo Raspadori a portare in vantaggio il Sassuolo sul campo del Verona dopo la traversa colpita da Kalinic. Hellas in dieci poco prima dell’intervallo per l’espulsione per doppia ammonizione comminata a Miguel Veloso. In avvio di ripresa gli emiliani trovano il raddoppio con Djuricic che dopo un’ottima combinazione con Caputo batte Pandur. Zaccagni accorcia le distanze su calcio di rigore assegnato per un fallo di Toljan ai suoi danni. Traoré con un gran gol riporta avanti di due i neroverdi. A rendere vivace il finale ci pensa ancora Zaccagni che al 90′ sigla la rete del 2-3 con un pregevole tiro a giro che sorprende Consigli.

Подобрать психолога

kqg

Некоторые люди бегут от мира, обрывают с ним все связи.

Порою их обуревает желание создать

новый мир, совершенно не похожий на предыдущий.

Однако действительность объективна.

Тот, кто уверовал в персональную возможность преобразования мира, часто заканчивает сумасшествием.

Если же большая группа людей желает обеспечить себе счастье путем преобразования действительности, то скорее всего мы имеем дело с какой-либо

религией. Психологичные книги.

Когда наступает вечер, я возвращаюсь домой и вхожу в свою рабочую комнату.

На пороге я сбрасываю свои повседневные лохмотья, покрытые пылью

и грязью, облекаюсь в одежды царственные

и придворные. Одетый достойным образом, вступаю я

в собрание античных мужей.

Там, встреченный ими с любовью, я вкушаю ту пищу,

которая уготована единственно мне,

для которой я рожден. Там я не стесняюсь беседовать с ними и спрашивать у них объяснения их действий, и

они благосклонно мне отвечают.

В течение четырех часов я не испытываю никакой скуки.

Я забываю все огорчения, я не страшусь бедности,

и не пугает меня смерть. Весь целиком я переношусь в них.

Как продавать

So, I’ll take the ‘over’ in tonight’s matchup between a pair of league bottom-dwellers that have both cleared the 120-point scoring mark in three of their last four games. The NBA Matchups are an essential betting tool for the novice or professional, and it has so many features to follow. The NBA regular season spans six months, and it’s rare to see the league take a day off, so analyzing the matchups and betting trends is vital. The best way to handicap NBA games is through consistent research and watching the games. This can give you the ability to identify trends for future games or for live betting. Read up on our How To Bet NBA guide to help you get started or you can always check out NBA consensus picks for further guidance on how to handicap NBA odds today.

https://blast-wiki.win/index.php?title=Nba_professional_picks

Betting on the eventual winner of the NBA Finals is the most popular form of NBA futures betting. But, there are so many more options to take advantage of all season long than just who takes home the championship trophy in 2023. For example, this bonus has a 10x rollover. When you deposit $100, we will give you a bonus of $50. The rollover is 10x the deposit + bonus. Therefore: To get started with PointsBet intuitive sign-up process, click here. Once you have opened and funded your account, you are ready to place your bets on Tuesday’s NBA action. And if your first fixed odds bet loses, you will get a second chance with bet credits of up to $100. Come back the next day and repeat for your first five days as a valued PointsBet customer for a chance at collecting up to $500 in total bet credits.